Conventional Loan

The perfect loan to help you build your future.

Conventional loans have a higher bar for approval than other types of loans do. They tend to be good for borrowers with good credit and a low debt-to-income (DTI) ratio who can make a down payment of 20%, as this allows them to avoid paying for costly private mortgage insurance (PMI).

Save money each month. Automatic Mortgage Insurance Termination at 78 percent LTV.

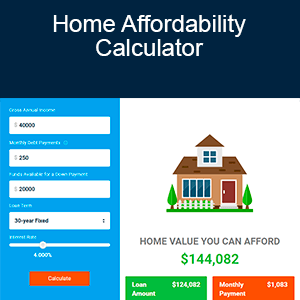

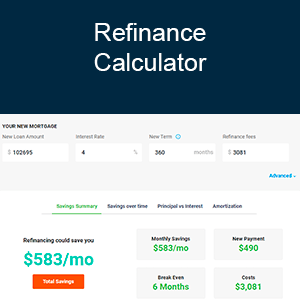

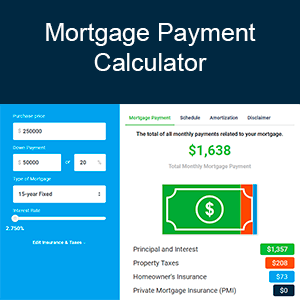

Mortgage Calculators

Need To Figure A Few Things Out?

Calculate

Calculate

Knowledge is power. Learn more about conventional loans.

What are the Conventional Loan Requirements?

To decide if you qualify for a Conventional Mortgage Loan, we will look at:

- Your income and your monthly expenses. Standard debt-to-income ratios are 28/36 for Conventional Loans. These ratios may be exceeded with compensation factors.

- Your credit history (this is important, but conventional loans’ credit standards are flexible). A FICO score of 620 or above is very helpful in obtaining approval.

- Your overall pattern rather than to individual problems you may have had.

To be eligible for a Conventional mortgage, your monthly housing costs (mortgage principal and interest, property taxes and insurance) must meet a specified percentage of your gross monthly income (28% ratio). Your credit background will also be considered. A minimum FICO credit score of 620 is generally required to obtain a Conventional approval. You must also have enough income to pay your housing costs plus all additional monthly debt (36% ratio). These percentages may be exceeded with compensating factors.

Conventional Loans require the home buyer to invest at least 5% – 20% of the sales price in cash for the down payment and closing costs. If the sales price is $100,000 for example, the home buyer must invest at least $5,000 – $20,000.

The interest rate for your home loan will be determined by the type of loan program that you qualify for and your credit score. You might be asking yourself “what is the formula to calculate interest rates?”. Interest rates are derived from Mortgage Backed Securities (MBS) which are commonly referred to “mortgage bonds”. The value of these bonds determines whether the interest rates rise or fall. Your final rate will determine your payment using the standard calculate mortgage payment formula. Please contact one of our loan officers to see what is today’s lending mortgage rate.

While Conventional Mortgage Guidelines allow you to purchase warrantable condos, planned unit developments, modular homes, manufactured homes, and 1-4 family residences. Conventional Loans can be used to finance primary residences, second homes and investment properties.

Criteria for Conventional loan approvals state that if you have been discharged from a Chapter 7 bankruptcy for four years or more, you are eligible to apply for an Conventional mortgage. If you have had a Chapter 13 bankruptcy, it must be documented that the your credit reputation has been re-established for at least two years to be eligible for a Conventional Loan Application.

The maximum amount for an Conventional Mortgage Loans are determined by:

Maximum loan amount: The maximum loan amount allowed for an Conventional Conforming Loan varies from county to county. The highest maximum Conventional Conforming right now is $729,750. The lowest maximum Conventional Mortgage amount available in any county is $510,400. To see what the limit is in the county in which you’re interested, visit the following site https://www.efanniemae.com/sf/refmaterials/loanlimits/. This site lists U.S. territories as well as states.

Maximum financing: Depending on the state where the property is located, the maximum Conventional Mortgage amount will be 80% – 95% of the appraised value of the home or its selling price, whichever is lower.